Static robust optimization involves the use of uncertainty sets to model the possible variations in problem parameters. By formulating optimization models that consider the worst-case scenario within these uncertainty sets, static robust optimization provides solutions that are robust against parameter variations.

We investigated various uncertainty sets and their connection to probabilistic guarantees, derived robust optimization formulations for different types of optimization models and presented numerical comparisons and real-world applications. Additionally, we studied the construction of uncertainty sets using polyhedral norms and emphasized the importance of integrating data and distributional information for better solutions.

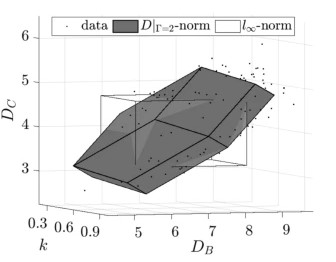

Uncertainty set